“The Exorbitant Privilege” — The Monetary Architecture of Empire

- Jeff Kellick

- May 3

- 38 min read

“I sincerely believe, with you, that banking establishments are more dangerous than standing armies; and that the principle of spending money to be paid by posterity, under the name of funding, is but swindling futurity on a large scale.”—Thomas Jefferson to John Taylor, May 28, 1816¹

Introduction: The Hidden Subsidy

In 1965, the French finance minister Valéry Giscard d’Estaing gave a name to the situation he had come to resent. The United States, alone among the nations of the earth, could print the currency in which the world’s debts were denominated. It could run trade deficits without consequence because the dollars it spent abroad were not lost to it — they returned to finance further American spending. It could consume more than it produced, import more than it exported, and borrow more than it earned, because the architecture of the post-war monetary system had made the dollar indispensable. Giscard called this arrangement le privilège exorbitant. The exorbitant privilege.²

Six years later, at a Group of Ten meeting in Rome in November of 1971, Treasury Secretary John Connally put the point less diplomatically to a gathering of European finance ministers. The United States had three months earlier severed the last link between the dollar and gold; European central banks were still scrambling to understand what the decision meant for their reserves. Connally’s famous reply condensed two centuries of Jeffersonian warning into ten words: “The dollar is our currency, but it’s your problem.”³

Connally was telling the truth as the United States understood it. The dollar was indeed America’s currency. The problem of maintaining its value — of continuing to accept paper that could be printed without limit in exchange for real goods and real labor — was increasingly the world’s. The system born in 1971 and matured across the following half-century has enabled every dimension of American global power this series has examined. It has financed the permanent warfare state. It has subsidized the permanent consumer deficit. It has built the largest military apparatus in human history and paid for it by taxing the savings of foreign citizens through the subtle mechanism of dollar inflation. It is the hidden half of the American empire, the half that does not appear in the evening news but without which the visible half would be impossible.

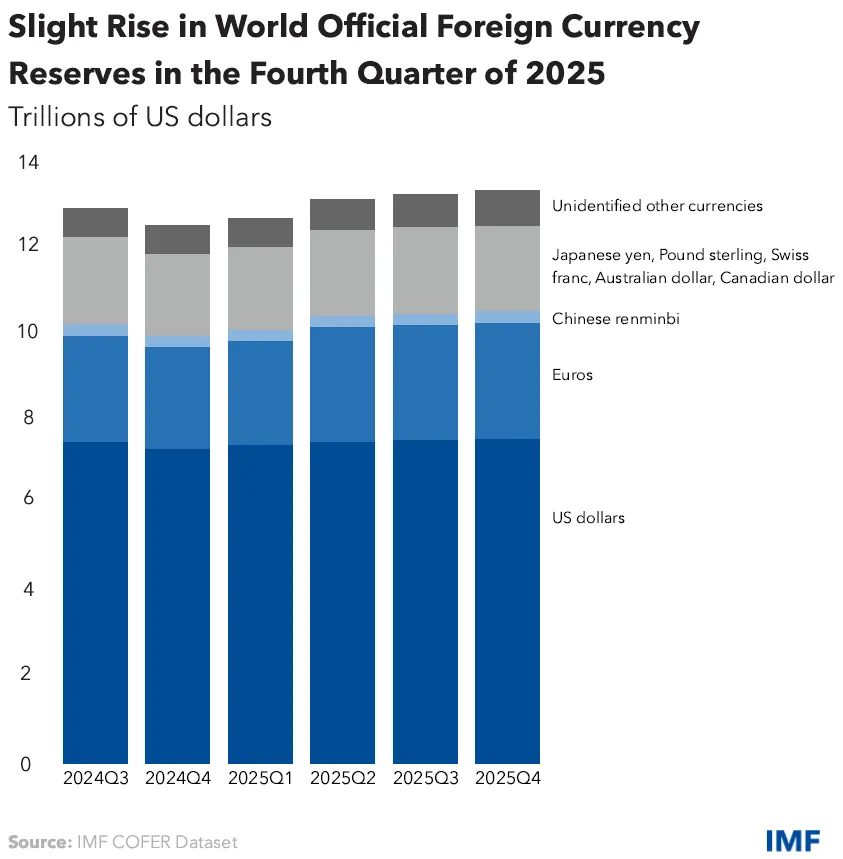

As of this writing in April 2026, the architecture is straining. The gross national debt of the United States crossed thirty-nine trillion dollars in early April, having grown by roughly two point eight trillion dollars over the preceding twelve months.⁴ Interest payments on that debt, according to the Congressional Budget Office, will exceed one trillion dollars in fiscal year 2026 for the first time in American history — a sum now approximately equal to the combined budgets of the Department of Defense and the Department of Education.⁵ Central banks around the world purchased eight hundred sixty-three tonnes of gold in 2025 — a modest pullback from the preceding three years, each of which exceeded one thousand tonnes, but a four-year cumulative total roughly twice the pre-2022 average. The World Gold Council describes the pattern as an unprecedented structural shift in reserve allocation.⁶ The share of the dollar in allocated global foreign exchange reserves stands at approximately fifty-seven percent, down from seventy-two percent at its peak in 2001.⁷ The decline is not collapse, but it is also not nothing. The architecture that made American empire possible is entering the phase in which its contradictions produce their consequences.

This article examines that architecture. What it is, how it was built, what it enables, and why it is no longer working the way its designers intended. The military empire traced throughout this series could not exist without the monetary system that finances it. Understanding that system is the precondition for understanding both the power the United States has exercised over three generations and the limits it is now beginning to encounter.

The Founders’ Monetary Vision

The men who wrote the Constitution had lived through an inflation. They knew, in the way that only personal experience teaches, what unbacked paper money did to a society. During the Revolutionary War, the Continental Congress had printed paper currency — the “Continental” — to finance the fight against Britain. By the war’s end, the Continental had become a synonym for worthlessness; the phrase “not worth a Continental” entered the American language and remained there for generations.⁸

When the Framers gathered in Philadelphia in 1787, they took care to ensure that such an experience would not be repeated through federal authority. Article I, Section 8 of the Constitution granted Congress the power “to coin Money, regulate the Value thereof.” The verb was chosen with precision. To coin, not to print. Money was a physical object with weight and metallic content. Article I, Section 10 prohibited the individual states from making “any Thing but gold and silver Coin a Tender in Payment of Debts.”⁹ The Constitution contained no grant of authority for paper currency, no provision for a central bank, and no acknowledgment that the federal government possessed any power to manipulate the money supply. What authority existed was to establish standards of weight and fineness for metallic coins.

The Coinage Act of 1792 operationalized this vision. The dollar was defined as a specific weight of silver — three hundred seventy-one and one-quarter grains of pure silver, to be precise — with gold defined in a fixed ratio of roughly fifteen to one. Citizens could bring bullion to the mint and have it struck into coins at no charge. The monetary standard was not something the government created. It was something the government recognized and maintained.¹⁰

The first great battle over whether the United States would adhere to this design came almost immediately. Alexander Hamilton, as Treasury Secretary, proposed a national bank modeled on the Bank of England. The First Bank of the United States was chartered in 1791 for a twenty-year term, over the strenuous opposition of Thomas Jefferson and James Madison. Jefferson’s warning to John Taylor of Caroline — quoted in the epigraph to this article — captures the objection in its essence: banking establishments are more dangerous than standing armies, and sovereign debt is swindling the future on a large scale.¹¹ The Bank’s charter expired in 1811 and was not renewed. A Second Bank of the United States was chartered in 1816; Andrew Jackson destroyed it in the 1830s, vetoing recharter in terms that explicitly connected central banking to aristocratic privilege and political corruption. Jackson’s veto message of July 10, 1832 remains one of the clearest statements in American political literature of why central banking and republican government are in tension: “It is to be regretted that the rich and powerful too often bend the acts of government to their selfish purposes... there are no necessary evils in government. Its evils exist only in its abuses.”¹²

For roughly eight decades between the death of the Second Bank in 1836 and the creation of the Federal Reserve in 1913, the United States operated without a central bank. The period was not free of panics or monetary disorder — nothing in the human condition produces such immunity — but it was the period in which the United States became the largest economy in the world, in which railroads spanned the continent, in which industrial capacity was built on a scale no prior civilization had achieved. Sound money did not prevent American prosperity. It accompanied it.

The classical gold standard under which the United States operated through the late nineteenth century imposed a particular discipline. Government spending was constrained by gold supply. Wars had to be paid for through taxation, through borrowing at rates the market would accept, or through the accumulated gold reserves of the Treasury. No president could simply decree that money would appear. The founders’ design, for all its imperfections, made certain kinds of folly arithmetically impossible. That is precisely what made it intolerable to those who wished to commit such folly.

The Creation of the Federal Reserve

The case for a central bank had always rested on the argument that private banking was unstable. The panics of 1893 and 1907 provided the political momentum that finally overrode Jacksonian resistance. In 1907, J.P. Morgan had personally organized a rescue of the American banking system, summoning other financiers to his library and directing the coordinated response that prevented a general collapse. The question, as reformers framed it, was whether a mature industrial economy should depend on the private decisions of a single banker. A lender of last resort was required. A central bank was needed. The existing arrangements were, in the phrase of the era, “obsolete.”¹³

The political problem was that the American public — informed by a century of rhetoric from Jefferson through Jackson to William Jennings Bryan — remained deeply suspicious of central banking. The solution was to design one without appearing to.

In November of 1910, six men boarded a private railcar in Hoboken, New Jersey, under conditions of carefully arranged secrecy. They were Senator Nelson Aldrich, chairman of the Senate Finance Committee and father-in-law of John D. Rockefeller Jr.; Paul Warburg of the banking house of Kuhn, Loeb and Company; Frank Vanderlip, president of the Rockefeller-aligned National City Bank of New York; Henry Davison, senior partner at J.P. Morgan; Assistant Treasury Secretary A. Piatt Andrew; and Arthur Shelton, Aldrich’s private secretary. Their destination was Jekyll Island, Georgia — a private retreat owned by a consortium of wealthy families. Their purpose was to draft legislation for a central bank.¹⁴

The participants used first names only. They told the press and fellow passengers that they were going duck hunting. The existence of the meeting was denied by participants for years afterward, until Frank Vanderlip confirmed it in his 1935 memoir and Paul Warburg acknowledged his role in his own writings. What emerged from Jekyll Island was the Aldrich Plan — renamed the Federal Reserve Act after Democratic victories in 1912 required cosmetic modifications to secure passage through a suspicious Congress.¹⁵

The Federal Reserve Act passed on December 23, 1913, during the Christmas recess, with many members already departed for their districts. President Wilson signed it into law the same day. The system it created was designed, as critics immediately observed, to look public while functioning privately. Twelve regional Federal Reserve banks, technically owned by their member commercial banks, would conduct the operational work of monetary policy. A Federal Reserve Board, appointed by the President, would provide political legitimacy. The institution was a central bank; it simply did not call itself one.¹⁶

The Austrian critique of central banking that developed in parallel with the Federal Reserve System — most fully in Ludwig von Mises’s The Theory of Money and Credit, published in German in 1912 — argued that the arrangement was worse than what it replaced. Private bank panics, in the Austrian view, were the market’s mechanism for liquidating bad credit decisions. A central bank could defer liquidation indefinitely by providing fresh credit, but deferral was not solution. The malinvestments accumulated. The distortions grew. The ultimate reckoning, when it came, would be more severe than the panics the Federal Reserve was supposedly designed to prevent.¹⁷ Murray Rothbard later summarized the indictment more pointedly: the Federal Reserve was not a bulwark against banking instability but a cartelization device that allowed the largest banks to expand credit in coordinated fashion and to share losses with taxpayers when the expansion failed.¹⁸

The test of these competing interpretations came quickly. The Federal Reserve was three years old when the United States entered the First World War. The pattern of its use would be established immediately, and it would prove not what its designers had advertised but what its critics had predicted.

War Finance and the Gold Retreat

Every major war fought by the United States since 1913 has been financed principally through monetary expansion rather than through taxation. This is not an accident of administrative convenience. It is the reason the Federal Reserve was created in the form it was created.

During the First World War, the Federal Reserve underwrote the Wilson administration’s financing needs through the purchase of government securities. The money supply roughly doubled between 1914 and 1920; wholesale prices roughly doubled as well.¹⁹ The gold standard was nominally maintained but effectively suspended for the duration. The pattern established in 1917 and 1918 would be the pattern of every subsequent American war: declare the emergency, expand the money supply, impose price controls to suppress the resulting inflation during the conflict, and allow the suppressed inflation to manifest in the years after the fighting ends. The taxpayer bears the cost eventually, but the cost arrives in the diffuse form of reduced purchasing power rather than the concentrated form of an honest tax bill. It is easier to pay for wars in this manner. It is also, the founders understood, the reason to avoid paying for them in this manner.

The interwar period produced the first major demonstration of what Austrian economists had predicted. The Federal Reserve’s expansion of credit during the 1920s — justified by reformers as maintaining price stability during a period of productivity gains that would otherwise have produced gentle deflation — fueled a massive asset bubble in the stock market and in real estate. When the bubble broke in October 1929, orthodox commentators blamed the gold standard. What had actually occurred, as Murray Rothbard documented in America’s Great Depression, was that the Fed’s credit expansion had produced a crash that would have required liquidation under any monetary system.²⁰ The response, under Hoover and then Roosevelt, was unprecedented government intervention. The most consequential monetary intervention came on April 5, 1933, when President Roosevelt signed Executive Order 6102.²¹

Executive Order 6102 required American citizens to surrender their gold coins, gold bullion, and gold certificates to the Federal Reserve System in exchange for paper dollars at the fixed rate of $20.67 per ounce. Failure to comply was punishable by a fine of up to ten thousand dollars or imprisonment for up to ten years. The following year, the Gold Reserve Act of 1934 revalued gold at $35 per ounce — effectively confiscating approximately forty percent of the real value of what Americans had just been compelled to surrender.²²

This was the moment at which the founders’ monetary system, as it applied to American citizens, was formally abandoned. A right that the Constitution had presumed and protected — the right to hold gold as money and to demand gold in payment — was abolished by executive order during an economic emergency and never restored. The right of American citizens to redeem paper dollars in gold would not return. (The prohibition on private gold ownership lasted forty-one years, until its repeal under President Ford in 1974.) The domestic dollar was now irredeemable fiat currency. Only foreign governments retained the theoretical right of gold redemption at $35 per ounce, through the gold window at the Federal Reserve Bank of New York.²³

This half-measure — fiat at home, gold redemption for foreign governments — would form the basis of the Bretton Woods system established in 1944 at the conference of Allied financial authorities held at the Mount Washington Hotel in New Hampshire. Under Bretton Woods, the dollar became the anchor of the international monetary system. Other major currencies were pegged to the dollar at fixed exchange rates. The dollar itself was pegged to gold at $35 per ounce, redeemable only by foreign governments. The United States held approximately twenty thousand metric tons of gold at the war’s end — more than half the world’s monetary gold supply — and the system worked because American production capacity and American gold reserves combined to make the arrangement credible.²⁴

It was not to last. The economist Robert Triffin identified the structural problem in 1960 in what became known as Triffin’s Dilemma: for the dollar to serve as the world’s reserve currency, the United States had to supply the world with dollars, which required running persistent balance-of-payments deficits. But running those deficits meant accumulating obligations in excess of the gold reserves supposedly backing them. Eventually, the world would hold more dollars than the United States had gold. At that point, the fixed exchange rate of $35 per ounce became a fiction, and the system became unstable.²⁵

Triffin’s Dilemma was not merely theoretical. By the late 1960s, Vietnam War spending and Great Society expenditures had inflated the dollar supply while American gold reserves contracted. France under Charles de Gaulle led the movement to call the American bluff, systematically converting dollar holdings to gold and shipping the metal home across the Atlantic in cargo ships. De Gaulle understood what the founders would have recognized immediately: a government that can pay its debts in paper it prints has a privilege no other entity possesses, and is constrained by no discipline external to its own restraint.²⁶

The Nixon Shock and the Fiat Era

By the summer of 1971, American gold reserves had fallen from twenty thousand metric tons at the war’s end to roughly eighty-one hundred tons. The remaining gold would cover only a fraction of outstanding dollar obligations held abroad. Britain requested three billion dollars’ worth of gold be transferred from Fort Knox in preparation for redemption. Switzerland and the Netherlands were preparing similar demands. The run on American gold that Triffin had predicted was underway.²⁷

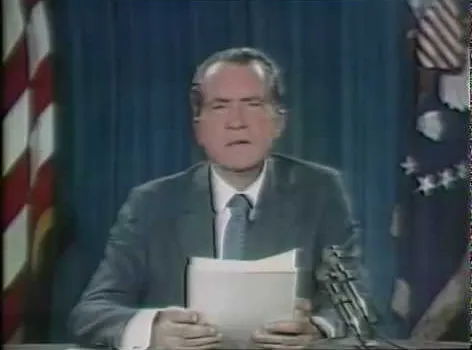

On the evening of Sunday, August 15, 1971, President Richard Nixon addressed the nation in a prime-time broadcast. Among several announcements in what his administration called the “New Economic Policy,” he included a single sentence that would reshape the international monetary order: the United States would “suspend temporarily the convertibility of the dollar into gold or other reserve assets.”²⁸ The announcement was presented as an emergency measure necessitated by international speculators. It was permanent. The gold window was never reopened. The dollar became, from that Sunday evening forward, a purely fiat currency — a promise of nothing beyond the promise itself.

The immediate consequences were everything the founders had feared from unbacked paper money. The dollar lost approximately a third of its value against major currencies between 1971 and 1973. Inflation, which had been gradually accelerating through the 1960s, surged into double digits in the mid-1970s. The stagflation of that decade — simultaneous high inflation and high unemployment, an outcome orthodox Keynesian economics had declared impossible — was the predictable result of a monetary system in which the discipline of gold had been removed and replaced with nothing. By 1980, the dollar had lost more than half its 1971 purchasing power.²⁹

The deeper consequence, however, was not the inflation of the 1970s but the structural change that inflation concealed. The last constitutional constraint on federal spending had been removed. Under the gold standard in any of its forms, the ability of the federal government to finance itself was ultimately limited by the willingness of citizens and foreign holders to accept its promises. A government that exceeded prudence would find itself rationed by the market through higher interest rates or through redemption of its notes into gold. Under the pure fiat system that emerged after 1971, the Federal Reserve could always, at least in theory, purchase whatever quantity of government debt was required. There was no external referee. There was only the question of whether, and when, the world would lose confidence in the dollar altogether.

The founders’ vision of constitutional money — the vision of Jefferson and Jackson, of the text of Article I — was fully abandoned on August 15, 1971. It has not been restored. Every American born since that date has lived entirely within a monetary system that has no constitutional foundation, no statutory limit, and no historical precedent for long-term stability. The question that hangs over the subsequent half-century is not whether such a system can work. It has worked, for fifty-five years and counting. The question is what has made it work, and whether the forces that have sustained it are beginning to fail.

The Multi-Pillar Architecture of Dollar Hegemony

A common explanation of what has allowed the dollar to function as a pure fiat currency for more than half a century centers on a single institution: the arrangement, negotiated in the mid-1970s between the United States and the Saudi government, under which oil would be priced and settled in dollars. This explanation is not wrong. It is incomplete. The dollar system is a multi-pillar structure in which the Saudi arrangement was one important element among several. Understanding the architecture requires examining each of the pillars that hold it up. Not all of them are vulnerable. Not all of them are strong. The question of whether the system will continue to function is the question of whether the pillars can continue to bear the load.

The Oil Pricing Arrangements

The first and most discussed pillar is the arrangement worked out between the Nixon administration and the Saudi government following the 1973 oil embargo. In July 1974, Treasury Secretary William Simon — a former Salomon Brothers bond trader whom Nixon had sent with instructions that there was, as internal documents obtained by Bloomberg through Freedom of Information Act litigation in 2016 later showed, “simply no coming back empty-handed” — spent four days in Jeddah negotiating what became the foundation of Saudi-American monetary cooperation.³⁰

The public component of what emerged was modest: a framework for economic cooperation, military sales, and technical assistance. The substantive component was kept secret for forty-one years. Saudi Arabia would price its oil in dollars and would recycle the resulting surpluses into United States Treasury securities through a special “add-on” facility that bypassed normal auction procedures, allowing the Saudis to purchase Treasuries without revealing the size or timing of their holdings. The arrangement was not a treaty. It was not debated in Congress. King Faisal’s one demand was that the purchases remain, in the language of the Bloomberg documentation, “strictly secret.” Saudi holdings were accordingly buried in Treasury reporting under the generic category “oil exporters” alongside fourteen other nations for four decades, until forced disclosure in 2016.³¹

The broader OPEC membership generally followed Saudi practice. Oil, across most of the international market, became dollar-invoiced. Nations that wished to purchase oil had to first acquire dollars. This created a structural source of demand for American currency that had nothing to do with the strength of the American economy or the productivity of American industry. The arrangement persists, in modified form, to the present day.

It is worth being precise about what the arrangement is and is not. The “petrodollar pact” has, in recent years, been the subject of various inaccurate claims in public discussion — including claims that the arrangement took the form of a formal fifty-year treaty that expired in June of 2024. No such treaty exists. The arrangements were informal, evolved through practice and through successor agreements over the decades, and involve multiple bilateral understandings that do not sit in a single document with an expiration date. Recognition of this does not diminish the importance of the oil-pricing pillar. It simply requires accurate description.

The Treasury Market

The second pillar is the depth and liquidity of the market for United States government debt. The Treasury market is by a substantial margin the largest and most liquid sovereign debt market in the world. Central banks hold Treasuries not merely because of oil-pricing arrangements but because Treasuries are the asset that can be bought and sold in virtually any quantity, at virtually any time, with minimal transaction cost. When a central bank needs to manage its reserves — to intervene in currency markets, to cushion against shocks, to respond to domestic banking stress — the Treasury market is the only instrument of sufficient scale. No other sovereign issuer produces enough debt, with enough reliability, across enough maturities, to serve this function.

This pillar is partly a function of American economic size; partly a function of the fiscal history that has made United States government debt credible; and partly a consequence of the network effects that lock in an incumbent reserve asset. It is the pillar least dependent on oil, least dependent on military power, and arguably the hardest to displace. Even if the dollar’s share of global reserves continues to decline, the Treasury market’s functional role is not easily replaced.

Legal-Tender Privilege and Network Effects

The third pillar is the dollar’s role in international transactions that have nothing to do with the United States directly. According to data compiled by the Atlantic Council’s Dollar Dominance Monitor, the dollar is involved in approximately eighty-eight percent of all foreign exchange transactions globally.³² When a Korean firm pays a Brazilian supplier, the transaction frequently routes through dollars — not because either party chose to do so, but because the correspondent banking system and the infrastructure of international finance have been built on dollar rails. The euro is used for roughly fifty-four percent of export invoicing in some measures; the dollar is used for over half. These figures represent network effects that have accumulated over eighty years. Switching costs are enormous. The first mover away from the dollar pays a substantial cost; the hundredth mover pays very little. This asymmetry slows change dramatically.

Federal Reserve Credit Expansion

The fourth pillar is the ability of the Federal Reserve to expand the dollar supply essentially without limit. Quantitative easing during the 2008 financial crisis and during the 2020 pandemic demonstrated that the Fed could purchase trillions of dollars of government debt and private securities without producing immediate collapse. This capacity underwrites both domestic financial stability and federal deficit financing. It is the mechanism that allows the Treasury to issue debt beyond what private markets would otherwise absorb at current interest rates. The Federal Reserve’s balance sheet expanded from under one trillion dollars before 2008 to approximately nine trillion at its peak in 2022, and remains near seven trillion today.³³ The constraint on this expansion is not law. It is inflation — the point at which the expansion of dollars outruns the growth of goods and services and the currency begins to lose value faster than citizens will tolerate.

Military Power

The fifth pillar is the American military. The relationship between military power and the dollar system has been the subject of considerable analysis, some of it reductive. Military dominance does underwrite the stability of international trade routes, the oil flows that the dollar-pricing arrangement depends upon, and the credibility of American security commitments that make foreign governments willing to hold American debt. It also provides a crucial counterfactual: nations are more reluctant to challenge American monetary arrangements directly because the United States possesses the capacity to respond in multiple theaters.

It is important, however, not to confuse the relationship between military power and monetary power with simple cause-and-effect. The two systems are mutually reinforcing. Military power helps sustain the dollar system; the dollar system finances military power; the reinforcement runs in both directions and has compounded over decades. But neither produces the other by itself. The dollar system would not survive the collapse of American military capacity, but American military capacity cannot, by itself, save a monetary system that is losing credibility on other grounds. This is worth keeping in mind when considering the present moment.

The five pillars reinforce each other. Weakening any one does not collapse the system. Weakening several simultaneously might. The question of whether the system will continue to function in its current form is the question of whether the erosion currently underway on multiple pillars can proceed indefinitely without cumulative consequences — or whether, at some point, the reinforcing relationships that have sustained the dollar for half a century begin to run in reverse.

The Weaponization of the Dollar

For most of the post-Bretton Woods period, the dollar system was enforced primarily through inducement rather than coercion. Foreign governments and central banks held dollars because dollars were useful, and because using dollars produced access to American markets, American investment, and American security guarantees. The costs of the arrangement — the gradual inflation that transferred purchasing power from foreign savers to the American Treasury — were real but diffuse, and they were tolerable given the benefits of participation.

Beginning in the late 1990s and accelerating dramatically in the 2000s and 2010s, the United States began to weaponize the dollar system directly. The instrument was the sanctions regime, and the mechanism was the fact that virtually all large-scale international finance flowed through systems that required dollar access.

The core infrastructure was SWIFT — the Society for Worldwide Interbank Financial Telecommunication — a Belgian cooperative through which international banks communicate transaction instructions. SWIFT was, in principle, a neutral utility. In practice, it was subject to American political pressure, and from the mid-2000s forward, the United States used that pressure aggressively. In 2012 and again in 2018, the United States forced SWIFT to exclude Iranian banks, effectively cutting Iran off from the international financial system. The mechanism was simple: any bank that used dollar correspondent relationships — which meant virtually every major bank in the world — had to comply with American sanctions or lose its dollar access. Secondary sanctions extended the reach further, punishing third parties who traded with sanctioned entities. A French bank doing business with Iran could be fined billions of dollars by American authorities; this was not theoretical, as BNP Paribas discovered in 2014 when it agreed to pay nearly nine billion dollars to settle sanctions violations.³⁴

The dollar system, by the 2010s, had become an instrument of American policy enforcement. Nations that displeased Washington could find themselves cut off from global commerce; nations that complied with American demands could continue to participate.

The decisive escalation came in February 2022. Within days of the Russian invasion of Ukraine, the United States and its European allies took a series of actions without precedent in the history of modern finance. Major Russian banks were excluded from SWIFT. Russian central bank reserves held in Western financial institutions — approximately three hundred billion dollars — were frozen. For the first time, the monetary reserves of a major sovereign power were rendered inaccessible as a consequence of that power’s foreign policy.³⁵

The technical justification for the freeze was the invasion of Ukraine; the strategic implication was far broader. Every central bank in the world watched what had been done to the Russian reserves. Every central bank understood, from that point forward, that holding dollar reserves was conditional on American political approval. A nation whose foreign policy diverged from American preferences could no longer assume that its sovereign savings were secure. The dollar system was not merely a convenience; it was now revealed as an instrument of political discipline.

This recognition produced the most significant shift in central bank behavior observed in the post-war period. The purchases of gold that followed the Russian reserve freeze are discussed in the next section. What should be noted here is the structural implication. The designers of the dollar system in the 1940s and the negotiators of the oil-pricing arrangements in the 1970s had relied on the tacit assumption that dollar reserves were functionally equivalent to real assets — that paper claims on the United States Treasury were as good as gold. The 2022 freezes demonstrated, before the watching governments of the earth, that this assumption was conditional rather than absolute. The instruments of American power had been used to discipline a sovereign actor. They could, in principle, be used to discipline any sovereign actor. The calculation of every reserve manager in the world changed accordingly.

The De-Dollarization Response

What has followed is a slow, structural shift in the composition of global reserves — not a collapse of the dollar, but a hedge against its increasing political conditionality. The data must be handled honestly, because rhetoric on this subject has at times exceeded the evidence.

The International Monetary Fund’s Currency Composition of Official Foreign Exchange Reserves — the COFER dataset — reports the dollar’s share of allocated global reserves at approximately fifty-seven percent as of the most recent release, down from a peak of seventy-two percent in 2001.³⁶ The decline has been gradual but persistent. The euro’s share has risen to approximately twenty-one percent. The Chinese renminbi remains at approximately two percent, despite considerable official Chinese effort to promote its international use — reflecting the fact that reserve currencies are made by market adoption, not by political ambition. The Swiss franc has seen disproportionate growth in recent quarters, quadrupling its share to roughly one percent in the two years since the Russian reserve freeze — a small share of the total, but a meaningful signal about the direction of reserve manager preferences.³⁷

More telling than the currency reserve data is the behavior of central banks in the gold market. According to the World Gold Council, central banks purchased eight hundred sixty-three tonnes of gold in 2025. That figure represented a moderation from the preceding three years — 2022, 2023, and 2024 each saw central bank purchases above one thousand tonnes, the longest sustained buying streak in modern record. Even with 2025’s pullback, the four-year cumulative total represents central bank demand at approximately twice the pre-2022 average.³⁸ These are not retail transactions. They are deliberate policy decisions by sovereign institutions to diversify away from dollar-denominated assets. The purchases are distributed across more than forty central banks; they are largely price-insensitive, meaning central banks have continued to buy even as gold has risen to record levels above four thousand dollars per ounce in 2026; and they show no sign of reversing. Combined gold holdings of the BRICS-plus nations — the original Brazil-Russia-India-China-South Africa group, joined in 2024 by Egypt, Ethiopia, Iran, and the United Arab Emirates, with Indonesia adding in early 2025 — have risen from eleven point two percent of global central bank gold to approximately seventeen point four percent, a structural shift of major proportions.³⁹

The BRICS-plus expansion itself deserves note. The group now represents approximately forty-six percent of the world’s population and roughly thirty-seven percent of global GDP by purchasing power parity. Internal BRICS discussions of a shared settlement currency or gold-backed common unit have produced considerable publicity but limited substantive progress, largely because the members — particularly China and India — have their own rivalries and their own monetary interests. What the BRICS expansion does provide is a framework for bilateral trade in local currencies, infrastructure for non-dollar payment settlement, and a political alignment around the principle of reducing exposure to American financial infrastructure.⁴⁰

The honest summary is this: the dollar is not being dethroned on any time horizon that current policymakers would recognize as short. Its share of global reserves is declining at perhaps one percentage point per year on average, with some acceleration since 2022. It remains overwhelmingly dominant in trade invoicing, international financing, and foreign exchange transactions. No credible alternative currency exists that possesses the combination of liquidity, political stability, and institutional depth that the dollar retains. The observation that seventy-three percent of central bankers surveyed by the World Gold Council in 2025 expect the dollar’s share to continue declining over the next five years describes a direction of travel, not an imminent arrival.⁴¹

What de-dollarization does narrow is American fiscal room for error. When the dollar’s global share was seventy-two percent and still rising, the United States could run substantial deficits confident that foreign demand for Treasuries would absorb the issuance at low yields. At fifty-seven percent and falling, that confidence is not what it was. The costs of American fiscal profligacy are beginning to return to the American taxpayer in the form of higher interest payments, which brings us to the most immediately pressing consequence of the architecture this article has described.

The Debt Trap

As of early April 2026, the gross national debt of the United States stands at approximately thirty-nine trillion dollars. To place that figure in scale: it represents roughly one hundred fourteen thousand dollars per person, or two hundred eighty-nine thousand dollars per household.⁴² Over the preceding twelve months, the debt grew by approximately two point seven seven trillion dollars — an average daily increase of seven point five eight billion dollars, or roughly eighty-seven thousand six hundred dollars per second.⁴³ The debt is currently on a trajectory to cross forty trillion dollars before the end of the summer.

Interest payments are now the most rapidly growing line item in the federal budget. For the first half of fiscal year 2026 — October 2025 through March 2026 — the federal government paid approximately five hundred twenty-nine billion dollars in interest on the national debt. This represents a monthly run rate of approximately eighty-eight billion dollars, or twenty-two billion dollars per week. Annualized, interest payments are on track to exceed one trillion dollars in fiscal year 2026 for the first time in American history.⁴⁴ A comparison recently noted by the Congressional Budget Office brings this figure into focus: interest on the national debt now exceeds the combined budgets of the Department of Defense and the Department of Education.⁴⁵ Viewed another way, the United States now spends more servicing its accumulated obligations than it spends to field the largest military in human history.

The Congressional Budget Office’s projections are more ominous. Under current law, net interest payments are expected to total sixteen point two trillion dollars over the coming decade, rising from one trillion dollars in 2026 to approximately two point one trillion dollars in 2036.⁴⁶ These projections assume no recession, no financial crisis, no loss of market confidence, no acceleration of de-dollarization. They assume, in other words, that the favorable conditions that have prevailed for half a century will continue indefinitely. The projections do not survive contact with any less benign assumption.

Under the classical gold standard that the founders established, debt of this kind could not have accumulated. Government borrowing was constrained by gold supply and by the willingness of private lenders to accept sovereign paper at prevailing market rates. A government that attempted to exceed its prudent borrowing capacity would find interest rates rising and gold departing the Treasury. The discipline was external, impersonal, and impossible to evade through political manipulation.

Under the fiat system that has prevailed since 1971, the constraint is different. The Federal Reserve can, in principle, purchase any quantity of government debt, at any interest rate, for any duration. The limit on this capacity is not arithmetic. It is inflation — the point at which the expansion of dollars outruns the growth of goods and services, and the currency begins to lose value faster than holders will tolerate. The United States has not reached this limit. But the pandemic-era monetary expansion of 2020 and 2021 produced the most sustained inflation of the post-war period, and the Federal Reserve’s response — raising interest rates from effectively zero to over five percent — revealed how costly the adjustment becomes when it finally arrives. At the new interest rate environment, the servicing cost of the accumulated debt is approximately three times what it was five years ago, and the servicing cost is now itself the fastest-growing component of the debt.⁴⁷

The Austrian economists who predicted this outcome across the twentieth century were not prophetic; they were applying consistent principles to foreseeable circumstances. Ludwig von Mises identified, in The Theory of Money and Credit, two terminal paths for fiat monetary systems: an eventual return to sound money through deliberate policy, or a collapse of the currency through accelerating inflation and loss of confidence.⁴⁸ Neither is painless. Neither is a likely outcome in the near term; the United States retains considerable room to continue extending the current trajectory. But the trajectory is not indefinitely extendable, and the question that confronts the country is not whether a reckoning arrives but when, and in what form, it does.

The military implications bear emphasis. The empire traced throughout this series is financed by the capacity to borrow without apparent constraint. If interest rates remain at current levels — which is already producing the interest burden described — the fiscal room for discretionary spending will narrow every year. Military budgets will increasingly compete with debt service for shrinking portions of a federal budget dominated by entitlement programs and interest payments. At some point, strategic retrenchment ceases to be an ideological preference; it becomes an arithmetic requirement. The empire will not be ended by a popular movement for restraint. It will be ended by the creditors.

Alternatives Under Discussion

Among those who have recognized the architecture this article has described, several alternatives have been proposed.

The Austrian tradition, represented most fully in the writings of Mises, Rothbard, and Friedrich Hayek, argues for a return to commodity money. The specific proposals vary — a restored gold standard, competing private currencies under a denationalized monetary regime, full-reserve banking that eliminates the credit-expansion capacity of fractional reserve systems — but the underlying logic is consistent: money should be a commodity that government recognizes rather than a fiat instrument that government creates. Ron Paul’s “End the Fed” movement has popularized these ideas in American political discourse, though they remain at the margins of mainstream debate.⁴⁹

A more recent alternative, emerging from the technological developments of the past fifteen years, is Bitcoin and the broader category of cryptocurrencies. Bitcoin offers a fixed supply — approximately twenty-one million units, never to be expanded — and decentralized issuance that removes the monetary sovereignty of any single government. Whether it constitutes a serious alternative to existing reserve currencies, or whether it will evolve into a speculative asset class within the existing monetary order, remains contested. Advocates argue that Bitcoin solves the fundamental problem that Austrian economists identified — the concentration of monetary authority in institutions that face political pressure to inflate — while critics note that Bitcoin’s volatility, its energy consumption, and its lack of the institutional infrastructure that supports existing currencies place significant obstacles in the path of widespread sovereign adoption. The technology exists. The political and institutional path to adoption is uncertain.⁵⁰

The transition problem, whatever alternative is preferred, is considerable. The debt that has accumulated cannot easily be serviced under a restored gold standard or under any system that limits federal money creation. Returning to sound money would require either partial default on existing obligations, sustained high taxation to retire the debt, or the hyperinflation that Mises identified as the terminal phase of the current system. None of these paths is politically attractive. The political system will almost certainly delay the reckoning as long as possible, which means delaying it until the reckoning arrives in a form that cannot be further delayed.

The founders’ insight, however, was more fundamental than any particular monetary mechanism. Jefferson understood that the power to create money and the power to create debt were not merely economic questions. They were political questions of the highest order, because they determined whether a government would be disciplined by its citizens or would acquire the capacity to impose its will without their consent. Sound money was a constraint on sovereign power. Fiat money removes that constraint. The warfare state and the welfare state alike are financed by the same capacity — to spend today and to tax tomorrow through the subtle mechanism of inflation. Those who favor either, or both, have a stake in perpetuating the current system. Those who wish the federal government to operate within constitutional limits have a stake in its reform.

The Interventionist Defense Answered

The strongest case for the current arrangement deserves presentation on its own terms before being evaluated.

That case, made by defenders of the status quo across the political spectrum, runs as follows. The dollar system has produced the longest period of general prosperity in human history. The Federal Reserve has prevented another Great Depression and has demonstrated, in 2008 and 2020, the capacity to respond to major financial shocks without permitting general collapse. Reserve currency status has benefited American consumers through cheaper imports and has benefited American businesses through lower borrowing costs. Sanctions enforcement through the dollar system has provided an alternative to military force in American foreign policy. No viable alternative currency exists that could replace the dollar without producing international monetary chaos. Proposals to return to the gold standard would impose deflationary pressure sufficient to trigger a severe depression. Serious people accept the current arrangements as imperfect but superior to the available alternatives.

Each of these claims should be answered on its merits.

The prosperity argument confuses correlation with cause. American prosperity has many sources — the productivity of American workers, the quality of American institutions, the geographical advantages of the continent, the benefits of accumulated human and physical capital, the peace among the great industrial powers for the longest period in modern history. Whether the dollar system has contributed to this prosperity or merely coincided with it is not obvious, and the evidence that inflation has transferred enormous wealth from savers to borrowers, from the middle class to financial institutions, from future generations to current office-holders, is substantial. The standard of living of the American median household, measured in real terms relative to median household income fifty years ago, is not unambiguously higher.

The Great Depression argument inverts the causation. The Federal Reserve produced the Great Depression through its credit expansion of the 1920s; its prevention of subsequent depressions has been achieved through further credit expansion that has papered over the bad debts of each crisis with newly created claims. This works until it stops working. The 2008 financial crisis and the 2020 pandemic response both required interventions of a scale that would have been politically inconceivable a generation earlier. Each intervention establishes the precedent for the next. The trajectory is toward ever-larger interventions in support of an ever-larger accumulated debt.

The cheap imports argument acknowledges what it claims as benefit: the dollar system has enabled Americans to consume more than they produce, and it has done so by gradually hollowing out American manufacturing capacity. The nation that sells its manufactured goods to the world and holds dollars in exchange does not thereby become wealthier; it becomes a client of the nation whose currency it is holding. This is a reversal of the relationship the founders envisioned, in which America would produce the real goods of civilization and other nations would aspire to American industrial success.

The sanctions-as-alternative-to-war argument deserves particular examination. In the cases of Iraq in the 1990s, of Cuba across sixty years, of Iran across four decades, of Venezuela in recent years, and of Russia since 2022, economic sanctions have produced humanitarian suffering at scale while failing to achieve their stated political objectives. Sanctions are not an alternative to war; they are a form of war that targets civilian populations rather than military ones. They rarely produce regime change. They frequently produce hardening of the regimes they target. They have, in the Russian case, accelerated the very de-dollarization that the American sanctioners wished to prevent. The claim that sanctions are preferable to military force rests on an assessment of their effectiveness that the historical record does not support.

The “no viable alternative” argument is true at present. It is true, however, because no alternative has been allowed to develop. The architecture described in this article has been defended aggressively, at substantial cost, for fifty years. The absence of a developed alternative is in part a product of that defense, not an independent fact of nature. The alternatives being constructed — Chinese settlement systems, BRICS payment infrastructure, central bank gold reserves, cryptocurrency networks — are being constructed precisely because participants in the current system have decided that continued dependence on it is no longer safe.

The founders’ judgment, finally, was that monetary power is political power. Jefferson opposed Hamilton’s bank on constitutional grounds and on grounds of political economy that have been vindicated by two subsequent centuries. Jackson destroyed the Second Bank because he understood what he was destroying: an institution that had acquired, through its control of credit, the capacity to reward its friends and punish its enemies on a scale that no republican government should tolerate. The current system is the system Jefferson and Jackson warned against, expanded to a scale they could not have imagined, financing an empire whose existence they would have regarded as incompatible with free government. That this system has delivered benefits alongside its costs does not settle the question. The question is whether the benefits can be sustained — and what is forfeited in their pursuit.

Conclusion: The Foundation Crumbles

Five observations follow from the architecture this article has described.

First, empire requires financing, and the dollar system provides it. The military establishment traced across the preceding seventeen articles of this series could not exist on the scale it has achieved without the capacity to borrow in a currency that the United States itself creates. The warfare state and the monetary state are not separate structures; they are components of a single system.

Second, fiat money removes the natural constraints on government that the founders built into the Constitution. A government that can pay its debts in currency it prints is constrained only by inflation and by loss of confidence. Both of these constraints operate eventually. Neither operates quickly enough to discipline day-to-day policy decisions that accumulate into decades of fiscal expansion.

Third, the exorbitant privilege is being eroded by its own weaponization. The United States has taught every central bank in the world that dollar reserves are conditional on American political approval. The response has been gradual but unmistakable: a shift toward gold, a search for alternative settlement mechanisms, a hedge against the possibility that the United States will, at some future moment, designate the holder as adversary.

Fourth, the accumulated debt has reached levels that have no historical precedent for peacetime. At nearly forty trillion dollars of gross debt and over one trillion dollars in annual interest payments, the United States is approaching the condition in which debt service will crowd out the discretionary spending on which the empire depends. This is not a matter of ideology. It is arithmetic.

Fifth, the monetary foundation of empire is unstable. De-dollarization is slow but real. The debt trajectory is unsustainable. The constraints that the United States has escaped for fifty years are returning. Strategic retrenchment will be forced — whether by policy choice, which is improbable, or by external circumstance, which is increasingly likely.

The founders, in their political economy as in their constitutional design, understood what modern policymakers have forgotten. Sound money constrains government. Fiat money enables government expansion without apparent cost, until the cost arrives. The warfare state and the welfare state are financed by the same mechanism; neither can be reformed while the mechanism remains intact. The liberty of the citizen is bound up with the soundness of the currency, because the authority to debase the currency is the authority to tax without consent. Jefferson’s warning to John Taylor — that banking establishments are more dangerous than standing armies — is not a quaint anachronism. It is the diagnosis of the condition in which Americans now find themselves.

The next article in this series examines the ongoing interventions that continue even as these constraints approach — Venezuela as a case study in the quiet wars that have persisted while public attention has been elsewhere, and the broader pattern of continued American activism that the arithmetic described in this article may finally begin to limit.

Self-Reflection Prompts

The Federal Reserve was created in secret meetings at Jekyll Island and passed during the Christmas recess of 1913. Its existence has accompanied every major monetary development of the last century — wars financed by inflation, the abandonment of gold in 1933 and again in 1971, the fiat dollar, the current debt trajectory. Does the institution’s origin and its subsequent record affect your assessment of its legitimacy as a component of American government?

The United States has run trade deficits continuously since 1975 — a situation that is possible only because the world accepts dollars in exchange for goods it could otherwise consume itself. What happens to the American standard of living when that acceptance ends? Has the arrangement actually benefited the American people, or has it hollowed out American productive capacity while enriching those who own financial assets?

The 2022 freezing of approximately three hundred billion dollars of Russian central bank reserves demonstrated that dollar holdings are conditional on American political approval. Every other central bank in the world observed this outcome. If you were the head of a central bank in a nation that might someday disagree with American foreign policy, how would you reassess your reserve allocation, and on what timeline?

The founders placed specific monetary restrictions in the Constitution: gold and silver coin as tender, no paper money, no central bank. The current monetary system bears no resemblance to what Article I prescribes. Does the Constitution still govern the monetary arrangements of the United States? If not, when was it amended, and by whom, and through what process?

At current interest rates, the debt service on the national debt is growing faster than any other category of federal spending. The Congressional Budget Office projects that interest payments will reach two point one trillion dollars annually by 2036. At some point, debt service will crowd out discretionary spending sufficient to force substantial reductions in military and other commitments. Is it preferable that such reductions occur by deliberate policy choice, or by external crisis?

Endnotes

¹ Thomas Jefferson to John Taylor of Caroline, May 28, 1816, in The Papers of Thomas Jefferson: Retirement Series, ed. J. Jefferson Looney (Princeton: Princeton University Press, 2012), Vol. 10.

² On Valéry Giscard d’Estaing’s coinage of “exorbitant privilege”: Barry Eichengreen, Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International Monetary System (New York: Oxford University Press, 2011), 4.

³ John Connally’s remarks to European finance ministers in Rome, November 1971, widely reported in contemporary press coverage and recounted in Eichengreen, Exorbitant Privilege, 61.

⁴ United States Congress Joint Economic Committee, Monthly Debt Update, April 2026, reporting gross national debt of $38.98 trillion as of April 3, 2026.

⁵ Congressional Budget Office, “Monthly Budget Review: March 2026,” released April 2026; on the comparison to DoD and Education budgets, see Fortune, “The U.S. government is spending $88 billion a month in interest on national debt,” April 9, 2026.

⁶ World Gold Council, “Gold Demand Trends: Q4 and Full Year 2025,” reporting 863 tonnes of central bank gold purchases in 2025, with the preceding three years (2022, 2023, and 2024) each exceeding 1,000 tonnes.

⁷ International Monetary Fund, Currency Composition of Official Foreign Exchange Reserves (COFER), Q4 2025 release.

⁸ On the Continental currency inflation: Murray N. Rothbard, A History of Money and Banking in the United States: The Colonial Era to World War II (Auburn, AL: Ludwig von Mises Institute, 2002), 59–68.

⁹ United States Constitution, Article I, Section 8 and Section 10.

¹⁰ Coinage Act of 1792, 1 Stat. 246 (April 2, 1792).

¹¹ Thomas Jefferson to John Taylor, May 28, 1816, as cited above.

¹² Andrew Jackson, Veto Message Regarding the Bank of the United States, July 10, 1832, available through the Avalon Project, Yale Law School.

¹³ On the Panic of 1907 and the political momentum for central banking: Robert F. Bruner and Sean D. Carr, The Panic of 1907: Lessons Learned from the Market’s Perfect Storm (Hoboken, NJ: Wiley, 2007).

¹⁴ On the Jekyll Island meeting: G. Edward Griffin, The Creature from Jekyll Island: A Second Look at the Federal Reserve, 5th ed. (Westlake Village, CA: American Media, 2010), chapters 1–2; Frank A. Vanderlip, From Farm Boy to Financier (New York: Appleton-Century, 1935), 210–219.

¹⁵ On Warburg’s role and the Aldrich Plan: Paul M. Warburg, The Federal Reserve System: Its Origin and Growth (New York: Macmillan, 1930), Vol. 1.

¹⁶ Federal Reserve Act, Pub. L. 63–43, 38 Stat. 251, signed December 23, 1913.

¹⁷ Ludwig von Mises, The Theory of Money and Credit, trans. H. E. Batson (Indianapolis: Liberty Fund, 1980; originally published in German, 1912).

¹⁸ Murray N. Rothbard, The Case Against the Fed (Auburn, AL: Ludwig von Mises Institute, 1994).

¹⁹ On World War I monetary expansion and price inflation: Milton Friedman and Anna J. Schwartz, A Monetary History of the United States, 1867–1960 (Princeton: Princeton University Press, 1963), 216–221.

²⁰ Murray N. Rothbard, America’s Great Depression, 5th ed. (Auburn, AL: Ludwig von Mises Institute, 2000).

²¹ Executive Order 6102, “Forbidding the Hoarding of Gold Coin, Gold Bullion, and Gold Certificates Within the Continental United States,” April 5, 1933.

²² Gold Reserve Act of 1934, 48 Stat. 337, revaluing gold at $35 per ounce.

²³ On the post-1933 domestic gold prohibition: Henry Mark Holzer, “How Americans Lost Their Right to Own Gold and Became Criminals in the Process,” Brooklyn Law Review 39, no. 3 (1973): 517–580.

²⁴ On the Bretton Woods system: Benn Steil, The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the Making of a New World Order (Princeton: Princeton University Press, 2013).

²⁵ Robert Triffin, Gold and the Dollar Crisis: The Future of Convertibility (New Haven: Yale University Press, 1960).

²⁶ On de Gaulle’s gold policy and the French challenge to the dollar: Francis J. Gavin, Gold, Dollars, and Power: The Politics of International Monetary Relations, 1958–1971 (Chapel Hill: University of North Carolina Press, 2004).

²⁷ Ibid., chapters 5–6.

²⁸ Richard M. Nixon, “Address to the Nation Outlining a New Economic Policy,” August 15, 1971, available through the American Presidency Project, University of California Santa Barbara.

²⁹ On 1970s inflation and dollar depreciation: William Greider, Secrets of the Temple: How the Federal Reserve Runs the Country (New York: Simon and Schuster, 1987).

³⁰ Andrea Wong, “The Untold Story Behind Saudi Arabia’s 41-Year U.S. Debt Secret,” Bloomberg, May 30, 2016, based on documents obtained through Freedom of Information Act litigation.

³¹ Ibid.

³² Atlantic Council GeoEconomics Center, Dollar Dominance Monitor, accessed April 2026.

³³ Federal Reserve Bank of St. Louis, Federal Reserve balance sheet data (FRED: WALCL), accessed April 2026.

³⁴ On the BNP Paribas settlement: U.S. Department of Justice, “BNP Paribas Agrees to Plead Guilty and to Pay $8.9 Billion for Illegally Processing Financial Transactions for Countries Subject to U.S. Economic Sanctions,” June 30, 2014.

³⁵ On the 2022 Russian sanctions and reserve freeze: U.S. Department of the Treasury, Office of Foreign Assets Control, sanctions announcements, February–March 2022; Adam Tooze, “Chartbook #135: Russia’s financial disarmament,” February 27, 2022.

³⁶ International Monetary Fund, COFER data, Q4 2025 release.

³⁷ On recent shifts in reserve composition: Atlantic Council, “Going for gold: Does the dollar’s declining share in global reserves matter?” December 23, 2025.

³⁸ World Gold Council, “Gold Demand Trends: Q4 and Full Year 2025”; on the four-year buying streak preceding 2025, World Gold Council, “Gold Demand Trends” annual reports for 2022, 2023, and 2024.

³⁹ On BRICS-plus gold reserves: EBC Financial Group analysis, “BRICS Gold Reserves Hit 17.4% as the Dollar’s Share Keeps Falling,” April 2026.

⁴⁰ On BRICS expansion and internal divisions: Council on Foreign Relations, “BRICS Backgrounder,” updated 2025.

⁴¹ World Gold Council, Central Bank Gold Reserves Survey 2025.

⁴² U.S. Congress Joint Economic Committee, Monthly Debt Update, April 2026.

⁴³ Ibid.

⁴⁴ Congressional Budget Office, “Monthly Budget Review: March 2026.”

⁴⁵ Fortune, “The U.S. government is spending $88 billion a month in interest on national debt,” April 9, 2026.

⁴⁶ Peter G. Peterson Foundation, “Interest Costs on the National Debt,” updated April 2026, citing CBO projections.

⁴⁷ On the effects of the 2022–2024 Federal Reserve rate increases on debt servicing: Peter G. Peterson Foundation, “Monthly Interest Tracker on the National Debt.”

⁴⁸ Mises, The Theory of Money and Credit, as cited above.

⁴⁹ Ron Paul, End the Fed (New York: Grand Central Publishing, 2009); Friedrich A. Hayek, Denationalisation of Money: The Argument Refined, 2nd ed. (London: Institute of Economic Affairs, 1978).

⁵⁰ On Bitcoin as monetary alternative: Saifedean Ammous, The Bitcoin Standard: The Decentralized Alternative to Central Banking (Hoboken, NJ: Wiley, 2018). On the challenges to sovereign adoption: Bank for International Settlements, Annual Economic Report 2023, chapter III.

Sources and Further Reading

Primary Documents:

U.S. Constitution, Article I, Sections 8 and 10

Coinage Act of 1792

Federal Reserve Act (December 23, 1913)

Executive Order 6102 (April 5, 1933)

Gold Reserve Act of 1934

Richard M. Nixon, Address to the Nation on Economic Policy (August 15, 1971)

International Monetary Fund, COFER data

Congressional Budget Office, Monthly Budget Review

U.S. Congress Joint Economic Committee, Monthly Debt Update

Essential Secondary Sources:

Ludwig von Mises, The Theory of Money and Credit (1912)

Murray N. Rothbard, What Has Government Done to Our Money? (1963)

Murray N. Rothbard, The Case Against the Fed (1994)

Murray N. Rothbard, America’s Great Depression (2000 ed.)

Henry Hazlitt, Economics in One Lesson (1946)

Henry Hazlitt, The Inflation Crisis, and How to Resolve It (1978)

Ron Paul, End the Fed (2009)

Friedrich A. Hayek, Denationalisation of Money (1978)

Barry Eichengreen, Exorbitant Privilege (2011)

Robert Triffin, Gold and the Dollar Crisis (1960)

Benn Steil, The Battle of Bretton Woods (2013)

Francis J. Gavin, Gold, Dollars, and Power (2004)

G. Edward Griffin, The Creature from Jekyll Island (2010 ed.)

Michael Hudson, Super Imperialism, revised ed. (2021)

Investigative Journalism:

Andrea Wong, “The Untold Story Behind Saudi Arabia’s 41-Year U.S. Debt Secret,” Bloomberg (May 30, 2016)

From Specified Authors:

Frédéric Bastiat, That Which Is Seen, and That Which Is Not Seen (1850)

Scott Horton, analysis at Antiwar.com and The Libertarian Institute

Ron Paul, ongoing commentary at the Ron Paul Institute for Peace and Prosperity

Comments